|

Not every personal loan fits the picture you are trying to paint. With some, the interest rates are high, and with others the documentation process is a complicated one - some problem or the other. But there’s one personal finance option that encompasses a host of benefits into an attractive package - the YES Bank Personal Loan. It is tailor made in a way to help you achieve your goals in no-time. Whether you want to take the long due abroad trip or send your kid to a prestigious B-school, the personal loan by YES Bank is a one-stop solution for all your needs. Provided at very reasonable interest rates, where paying back doesn’t seem like much of a struggle. The approval and disbursal process is very fast. Let’s take a tour of some of the other amazing features of this loan to help you take the right decision.

What are some Exciting Features of the YES Bank Personal Loan? YES Bank Personal Loan Interest Rate: Query about the interest rate is one of the prime concerns of borrower - that’s why we are addressing it first. YES Bank understands that paying back the personal loan takes a dig at 10-20% of the monthly income. Only an affordable interest rate won’t put so much financial pressure on you. Interest rate provided by YES Bank starts from 10.99% per annum. Loan Amount: Hefty loan amounts are provided by YES Bank so that the person doesn’t have to worry about finances while meeting his dream. If you have all the documents and an outstanding credit track record, you’ll be eligible for a higher loan amount. Collateral Free: The personal loan offered by YES Bank is unsecured in nature, that means the bank doesn’t ask for any collateral or securities to be pledged against it. All you have to do is just meet the eligibility criteria and the YES Bank personal loan is yours. Pre-payment or foreclosure Option: If you’ve had a food financial year - got a handsome bonus or made crazy incentive - YES Bank gives you the option to prepay your personal loan. However, you can prepay your loan only after you’ve finished paying 12 EMIs. How Can I get the Lowest YES Bank Personal Loan Interest Rate? Credit Score: As stated earlier, the YES Bank Personal Finance is a collateral free ( unsecured) loan. This implies that the bank doesn’t ask you to pledge any security in order to avail it. So you’ll be wondering on what basis will the bank trust you with the loan money. Heard of Credit Score? The bank checks your credit score before approving the personal loan. And a good credit score can help you procure the lowest interest rate from YES Bank. A score of 750 and above can fetch you the lowest YES Bank personal loan interest rate. Relationship with YES Bank: A good relationship with the bank is always a plus factor. If you have an existing relationship with YES Bank in terms of bank account or previous loan, chances are that it will give you a low rate of interest. Also, if you have opted for YES Bank personal loan finance option and serviced it well, even this can get you a low interest rate.

0 Comments

Buying a home is always on the wishlist of all those living in the hassles of rental accommodation. They must be wanting the freedom that those living in their own home enjoy. Thankfully, there are several lenders that provide home loans at attractive rates of interest. You can thus choose from different home loan interest rates and buy the property of your choice. So, what is the delay? Let’s check out the rates of top lenders that are dominating this space.

Home Loan SBI The country’s largest lender State Bank of India (SBI) provides home loans at variable rates of interest according to the loan amount. The rates also vary according to the gender and profession of an individual. As of now, SBI home loans are available at interest rates of 8.35%-9.05% per annum. Loans up to ₹30 lakh, above ₹30 lakh to 75 lakh and above ₹75 lakh can be granted at 8.35%-8.65%, 8.60%-8.90% and 8.70%-9.05%, respectively. Home Loan HDFC HDFC, like SBI, is also a prominent lender by offering customized home loans at variable interest rates. It also charges interest based on the loan amount, profession and gender. On the whole, HDFC provides at 8.40%-9.50% per annum. Applicants applying for loans up to ₹30 lakh would find the interest rates to be ranging from 8.40%-9.15% per annum. When the application goes for loans above ₹30 lakh to ₹75 lakh, the rates remain in the range of 8.75%-9.45% p.a. Once the application goes past ₹75 lakh, the interest rates come out as 8.80%-9.50%. Axis Bank Home Loan Axis Bank is also one of the leading home loan providers in India. The bank offers loans at attractive interest rates. Loans up to ₹30 lakh, up to ₹75 lakh and above ₹75 lakh can be given at 8.90%-8.95%, 9.05%-9.10% and 9.10%-9.15% per annum, respectively. ICICI Home Loan ICICI Bank offers fierce competition to its rivals in the home loan space. Loans up to ₹35 lakh, above ₹35 lakh to 75 lakh and above ₹75 lakh at 9.05%-9.10%, 9.15%-9.20% and 9.20%-9.30% p.a. So, these were some of the top lenders that exist in the home loan space. Let’s figure out the function of the Home Loan Calculator to make the right decision regarding the loan. How to Check the Function of Home Loan Calculator? You can check the function of the home loan calculator online and set your budget accordingly. The calculator helps compute the repayment variables. All that you need to do is to enter the loan amount, tenure and rate of interest in the EMI calculator. The calculator would then show the exact EMI amount, interest to be paid over the debt course, etc. If you check the calculator before taking a loan, you can be benefited greatly by knowing the repayment in advance. So, it won’t be difficult for you to make those subtle adjustments.  Home is the basic necessity for any individual and everyone wants to own their own home at some point in their lives. But not everyone is financially capable to buy his/her own home or land considering the hefty prices of the homes in our country. To help them financially and to make them able to achieve their dream home, banks and financial institutions of our country provide a facility known as Home Loan to the individuals who require it. Through this facility, they get the loan amount against the property as collateral or security.

Dewan Housing Finance Corporation (DHFL) is one of the top housing finance companies in India that provide various kinds of facilities ranging from home loans, plot loans, home construction loans, home extension loans, home renovation loans, and many others. The rate of interest offered by DHFL is quite competitive compared to the current financial market, also individuals get flexible tenure period for the repayment of the loan. In this article, you’ll get to know everything about the Home Loan DHFL and what are the features that make it one of the best options available. What are some Prominent Highlights of the Home Loan DHFL: The list of benefits that an individual get through the home loan by DHFL can go on and on. Below are some of the salient features that you can have a look at.

How to use the DHFL Home Loan calculator to estimate the EMI amount? With the help of the Home Loan calculator, you can easily get an estimate of your EMI amount that you’ll be paying over a period. For using it, you only need a few basic details which are the desired loan amount, rate of interest, and tenure period. By putting these details into the calculator, you will get the exact EMI amount for your desired loan amount. Eligibility Criteria for getting a Home Loan from DHFL: There are a few basic qualifications which an individual has to fulfill before getting the home loan facility. These are mentioned below.

An article published on Economic Times reads “Indians spend roughly 3 hours a day on smartphones.” With the Internet boom hitting India, there’s a considerable rise in the aspirations of people, who see a variety of products on the Internet from all over the world. This sets in a need to own those products, which can be a little over the top (expensive) sometimes. But don't worry, YES Bank credit cards can help you achieve your aspirations in no-time. They take the burden off yours shoulders by converting the total purchase price into affordable EMIs. Along with this, YES Bank credit cards are loaded with exciting offers and amazing reward structure. Let’s have a look at some of these credit cards and the offers that come along with them.

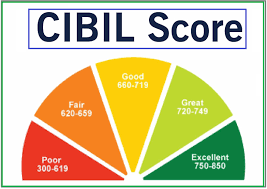

Yes First Exclusive Credit Card: It totally brags about it exclusivity and why shouldn’t it? It offers the best rewards and unmatched privileges that aren’t offered by any other credit card in India. Enjoy welcome benefits when you sign up for this credit card. You get 50000 reward points on your first transaction made within 90 days from the sign-up date. By the time when you renew your credit card, you can earn upto 40000 reward points on each renewal. On spending INR 20 lakh in a year using this credit card, you get 25000 Bonus reward points. These reward points can be redeemed for Flight or Hotel or Movie Ticket Booking of partner merchants or for exclusive catalogue of products. One reward point translates into INR 0.25. Adding more to its glory - avail complimentary membership of Taj InnerCircle Epicure (but only primary card holders can enjoy this). You also get free insurance coverage with this card. Yes First Preferred Credit Card This is a card meant for people who want to derive more value from day to day transactions rather than people who want to enjoy premium privileges. People who want exclusive and premium benefits should go with the above mentioned YES Bank credit card. Avail 50000 reward points as welcome benefit on your first transaction made within 90 days after signing up. A movie buff? Enjoy the delightful discount of 25% when you book movie tickets on BookMyShow using this YES Bank credit card. This card is highly protected and secured as it has the new Contactless technology, which protects you from skimming and counterfeiting. How to make YES Bank Credit Card Payment Online? If there’s a credit card bill payment due, make sure you pay it as soon as possible. If ignored, you will end up being subjected to excruciating interest rates and this amount keeps piling on, eventually, pushing you on the edge. This is the reason why YES Bank has a host of online payment services for the convenience of the customer. Below mentioned are some online payment modes through which you can make YES Bank credit card payment: NEFT/IMPS/RTGS: You can pay your bill by doing an NEFT/IMPS/RTGS transaction towards the Yes Bank Credit Card Account. How to go about this? It’s really simple, all you need to do is add YES BANK Credit Card as a beneficiary. Use IFSC code: YESB0CMSNOC and then transfer the amount to the Yes Bank Credit Card Account. Net Banking: Yes Bank account holders can register for the Net Banking facility and make the credit card payment. Yes PayApp: You can pay your YES Bank credit card bill from anywhere and anytime using the Yes PayApp which facilitates UPI payments. Yes Bank Mobile App: You can also make the Yes Bank Credit Card Payment by logging in to the mobile banking of Yes Bank App. And then use your saving bank account to pay the bill.  Let’s get to the basics first. CIBIL score is a three digit number assigned to individuals by the credit information company, TransUnion CIBIL, in order to help banks and NBFCs gauge the credit track record of the individual. Lenders make it a point to check CIBIL score before approving any loan requests. CIBIL score is checked to determine whether the individual has the capability to repay the loan or not.

You can’t board a flight without security check, right? Similarly, it’s hard to get a personal loan without getting frisked by CIBIL score .The reason being personal loans are unsecured loans, implying no securities need to be pledged in order to take the loan. So the banks have no other way to gain confidence in you other than checking your CIBIL score. But in practicality, banks do sometimes discount the CIBIL score check, only for their old and prime customers. It can also take a back seat when the loan amount is a small one and you have all the mandatory documents with you. How to check CIBIL Score for Free? You’ll be delighted to know that TransUnion Credit Information Bureau of India Limited gives everyone the opportunity to get their CIBIL report for free. All you have to do is follow the below mentioned steps:

However, if you want to check the credit score for more than once, you can’t do it for free. One more way is there, where you will have to pay for the subscription model by CIBIL which gives you CIBIL Score Report on a half-yearly and quarterly basis. Why is it Important to do a Credit Score Check? Availing Credit - In case of secured loans (home loans) and secured credit cards, the need for credit score can be discounted because banks ask you to submit collateral against it. In the event of default, the bank can simply seize your collateral in order to recover the loan. This is not the case with unsecured loans (personal loans) and secured credit cards. Here the bank grants you the loan on trust basis. The bank trusts you on the basis of your CIBIL score (credit score). In order to get loan approvals without any hassle, maintain a credit score of 750 and above. Credit Check: It helps you manage your finances by letting you check your credit track record in front of your eyes. You can spot where you are going wrong with your credit transactions. Once you’ve spotted these, you can rectify these errors by making payments for the same. Dispute Settlement: In case you have issues with some credit transactions or the scores assigned, you can always call for dispute settlement. Every credit information company has a dispute settlement wing who looks thoroughly into your complaint and makes changes accordingly. So a regular credit score check helps you being aware of your financials. 8/26/2019 How Can Interest Rate of Home Loan in Axis Bank Help You in Owning Your Dream Home?Read Now A home is much greater than the four walls and a roof, it’s a feeling. If you’re one of those individuals wanting to fulfill your dream of getting that feeling of your own home but afraid of the high-priced homes. It’s a bit tough for a large portion of our country’s population to buy their own homes by the one-time amount payment. To solve their problem, various banks and financial institutions provide the home loan facility. By this means, the individuals can borrow the needful amount to achieve their dream of home.

Axis Bank, one of the top financial institutions of India, also provides the home loan facility at a competitive rate of interest which you can repay in easy installments within your chosen tenure period. An individual can not only purchase the home or land with the loan amount but can also enjoy the services like home repair, home improvement, home extension, and other features. The thing which makes it stand out among all the loan options is the Interest rate of home loan in Axis Bank. In this article, we will talk about the various details about Axis Bank Home Loan. What features make Axis Bank Home Loan the best in the business? There are a few features that make the Axis Bank as one of the most reliable lenders in the market. All those features are mentioned below.

Eligibility Criteria for getting a Home Loan from the Axis Bank:

Wondering about the EMI amount that you will have to pay to repay the loan amount? Or want to calculate the amount so that you could know the exact portion of the monthly budget you have to keep aside for the repayment of your personal loan? Well, whatever your reasons are, there is this one and simple solution for all your doubts. A Personal Loan calculator is an answer to all your questions. With the help of a personal loan calculator, you can save yourself from all the petty calculations and make all those calculations in a quick and hassle-free manner.

The most prominent use of personal loan calculator; also known as EMI calculator is to assess the correct amount of monthly installments. It helps individuals to manage their budget according to their repayment capability so that the EMI of their loan amount wouldn’t burn a hole in their pocket in while repaying the loan. To use the personal loan calculator, an individual needs a few basic details such as the loan amount, rate of interest, and the tenure period. In this article, we will tell you about the proper usage of the calculator and its benefits. What are the details we need to use a personal loan calculator? Like we’ve told you previously that to use an EMI calculator, we need a few basic details that you can choose according to your need and repayment capability. Below are those details.

By putting all these above-mentioned details into the EMI calculator, your exact amount of EMI will be at your disposal within a second by which you can plan your personal loan in a better way. Also, you will get the total interest amount that you’ll be paying over your loan period. A personal loan EMI calculator is nearly flawless in its calculations, so you can sit back and trust it completely. Apart from this, you can calculate the EMI amount for infinite times, as it’s endlessly flexible. Trust is an important factor whether it is with regards to relationships or business. Banks trust you with the loan money on the basis of your CIBIL score. Trust, nowadays, is synonymous with CIBIL Score (atleast in respect to banking). CIBIL is extremely imperative in the case of personal loan. This is because personal loans are unsecured loans, which means they are given without pledging of any security or collateral. So the only way that the bank has confidence in you with its loan amount is the CIBIL Score. It is highly recommended for those who don’t care much about their credit profile, it’s high time you buck up. All of us have dreams and to be honest they can’t be fulfilled by just our savings. We will require personal loans to achieve them. And that is where maintaining a good CIBIL score for personal Loan will help.

Why maintaining a good CIBIL Score for Personal Loan is important? Credit Worthiness: Maintaining a good credit score gives your lender the assurance that you’ll repay the loan in time. It helps lenders assess your credit-worthiness. Whereas, a bad credit score will put you in a tough spot where the chances of you getting a loan is dicey. However, you might be able to get it on the grounds of some terms and conditions. High Loan Amount: A person with a high credit score can negotiate for a higher loan amount. On the other hand, this privilege is not applicable to a person with a low credit score. Here’s you incentive to receive more funds in your hand. Rate of Interest: Since time, being good has always an edge over being bad. Similarly, a good credit score puts you in a sweet spot with the bank. It puts you in a position where you can negotiate with your bank regarding the rate of interest. You can demand a low rate of interest if your credit score is extremely good. Processed with Ease: If you possess a good credit score, the bank approves your personal loan easily without any terms and conditions attached to it. Once it has a vivid picture of your credit health, the funds are released into your account in a short period of time. What is a good CIBIL Score for Personal Loan like? As discussed earlier, personal loans are unsecured loans unlike home loans. This leaves the banks to grant you loan only on the basis of your credit history, repayment of debts, credit card payments and number of ongoing loans. And all of this is determined on the basis of your credit score given by CIBIL. The credit score ranges from 300-900, with 300 being on the lower end and 900 representing the higher end. Let’s assume, if you have a credit score of 350, there’s no way the banks will accept your request for a personal loan. On the other hand, if you’ve a score of 750 and above, you’re likely to get the loan without any difficulties. A high credit score translates the fact that you’ve paid your credit card bills on time and your credit record is clean.  CIBIL scores are credit scores assigned by the Credit Information Bureau of India to individuals. This score shows the credit journey of an individual till the present date. It is like your financial report card which gives banks an idea about your credit behaviour. A good credit track record translates into easy loan or credit card approvals. Whereas, a bad credit track record can get you drenched in sweat while applying for loans or credit cards. CIBIL score ranges from 300-900, with 300 being the worst and 900 being the best. Banks generally prefer a score of 750 and above in case of loan disbursement to individuals.

What’s all the Hype about Checking CIBIL Score? You must be wondering what’s all the fuss about checking your CIBIL score. Well, it’s a valid concern if you’re looking to avail credit facilities from banks and NBFCs. CIBIL scores are extremely important when it comes to procuring unsecured loans (like personal loans) and credit cards. The reason being that these credit facilities are provided without submitting any collateral. So, the only point of reference of your credibility for the bank is your CIBIL score. Whereas in the case of loans with collateral (secured loans like home loans), CIBIL score can be discounted. The reason being on the event of defaulting in loan payment the bank seizes the collateral. However, the credit score in not totally discounted. Some banks adhere to strict checking of CIBIL score. Now you know why everyone is stressing on ‘check CIBIL score’. How to Get Free CIBIL Score? There are numerous ways to check CIBIL score. You can do it on CIBIL’s website or there are various other portals online that gives you free CIBIL score report or you can request for your credit score via Whatsapp or offline mode. All of these processes are very convenient and easy to use. Let’s go through a step by step navigation of these process to understand how to check CIBIL score. Check CIBIL score Offline: In case you’re not comfortable checking your CIBIL score online, you can opt for the offline mode. All you have to do is:

Through Whatsapp: Some financial technology companies gives you the luxury of viewing the credit score on Whatsapp. All you have to do is drop a message with your PAN card details on their Whatsapp number. Instantly, you’ll receive your credit score and information. This is how to check CIBIL score. What are you waiting for? Go, check your CIBIL score and get your loan & credit card demands get approved.  A personal loan helps you in unimaginable ways of getting out of the various financial emergencies. Whether you’re needing money for your child’s education or you’re trying to sort your financial situation for your abroad trip or you require money for the upcoming marriage, or any other financial emergent situations, A personal loan gets you out from any of them. If you’re facing any kind of these situations right now and looking for the various personal loan options in the current banking sector, then let us tell you why you should opt for an HDFC Bank personal loan and why it will be best for your needs.

HDFC Bank is the largest mortgage in India when it comes to the private banking sector banking spectrum. There are several features in the personal loan given by HDFC Bank which makes it suitable for everyone. Attractive interest rates, flexible tenure period, minimal documentation, quick disbursal of loan amount and many other features make HDFC bank personal loan worthy to have. But there are a few things which people don’t remember before taking the personal loan from any of the banks. Among those few things, the EMI amount is the most important thing to keep an eye on. EMI amount is the amount you have to pay every month while repaying the loan amount. If you won’t have a pre-estimation of it, then it can certainly burn a hole in your pocket in the future which will unnecessarily affect your monthly budget. So it’s better to have some calculation of it. For this purpose, we can use the HDFC Personal Loan Calculator. It is a magical tool for calculating the exact amount of EMI in an hassle-free manner. Details required to use the HDFC Personal Loan Calculator? To use the HDFC Personal Loan Calculator, we need a few basic and important details by which it will calculate the EMI on your loan. These details are as follows.

After filling out all the details in the calculator, you’ll get the EMI amount in the fraction of a second. Apart from this, you’ll also get the total interest you’ll pay over a period. The best thing about this calculator is it can be used by anyone in an hassle-free manner. Benefits of using HDFC Personal Loan Calculator: There are various advantages of using this EMI Calculator which are mentioned below.

|

Anika Sharma

|

RSS Feed

RSS Feed